.png)

Market Knowledge

FEBRUARY 2025 HOUSING MARKET UPDATE

March 3, 2025 Sales remain above long-term trends despite declines Inventory levels saw substantial year-over-year growth for the second ...

READ POSTBlogging has not been my strength and so this is officially a work in progress. I have some big plans for the blogging page in the foreseeable future so I ask for your patience as I venture into this side.

March 3, 2025 Sales remain above long-term trends despite declines Inventory levels saw substantial year-over-year growth for the second ...

READ POSTSupply levels improve in January Calgary, Alberta, February 3, 2025 – Following three consecutive years of limited supply choice, inventory ...

READ POST2024 marks another strong year for sales and price growth The year ended with 1,322 sales in December, a three per cent decline over ...

READ POSTDecember 2, 2024 Supply on the rise, but not across all price ranges As we transition into winter, Calgary's housing market is following ...

READ POSTTimes Are Tough, But Finding Low-Cost Fun Shouldn't Be Here Are Things To Do This Month FOR FREE Legacy’s ...

Home safety for trick or treaters As a responsible homeowner, making your property safe for young trick-or-treaters ...

Demand shifting to more affordable options

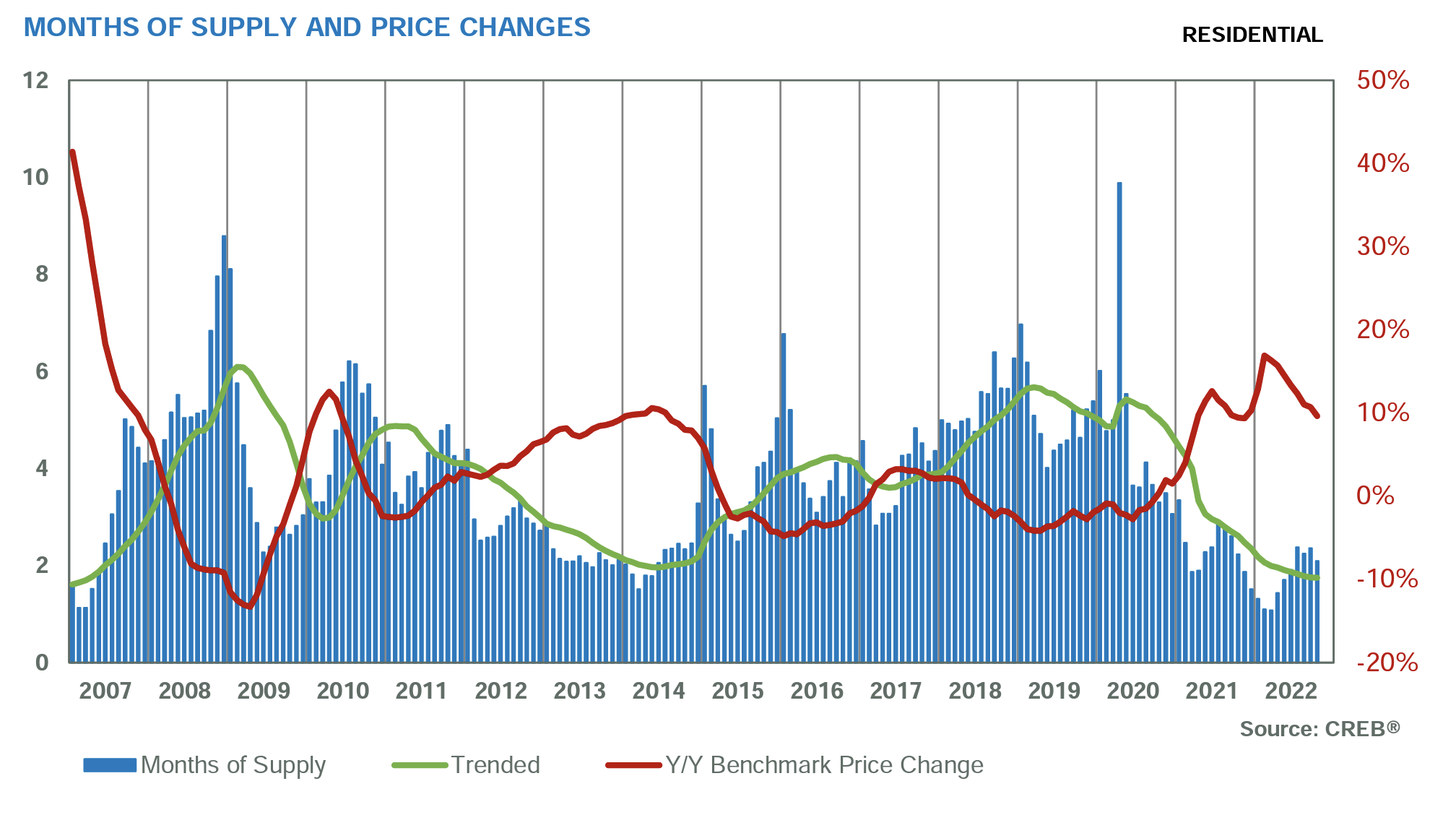

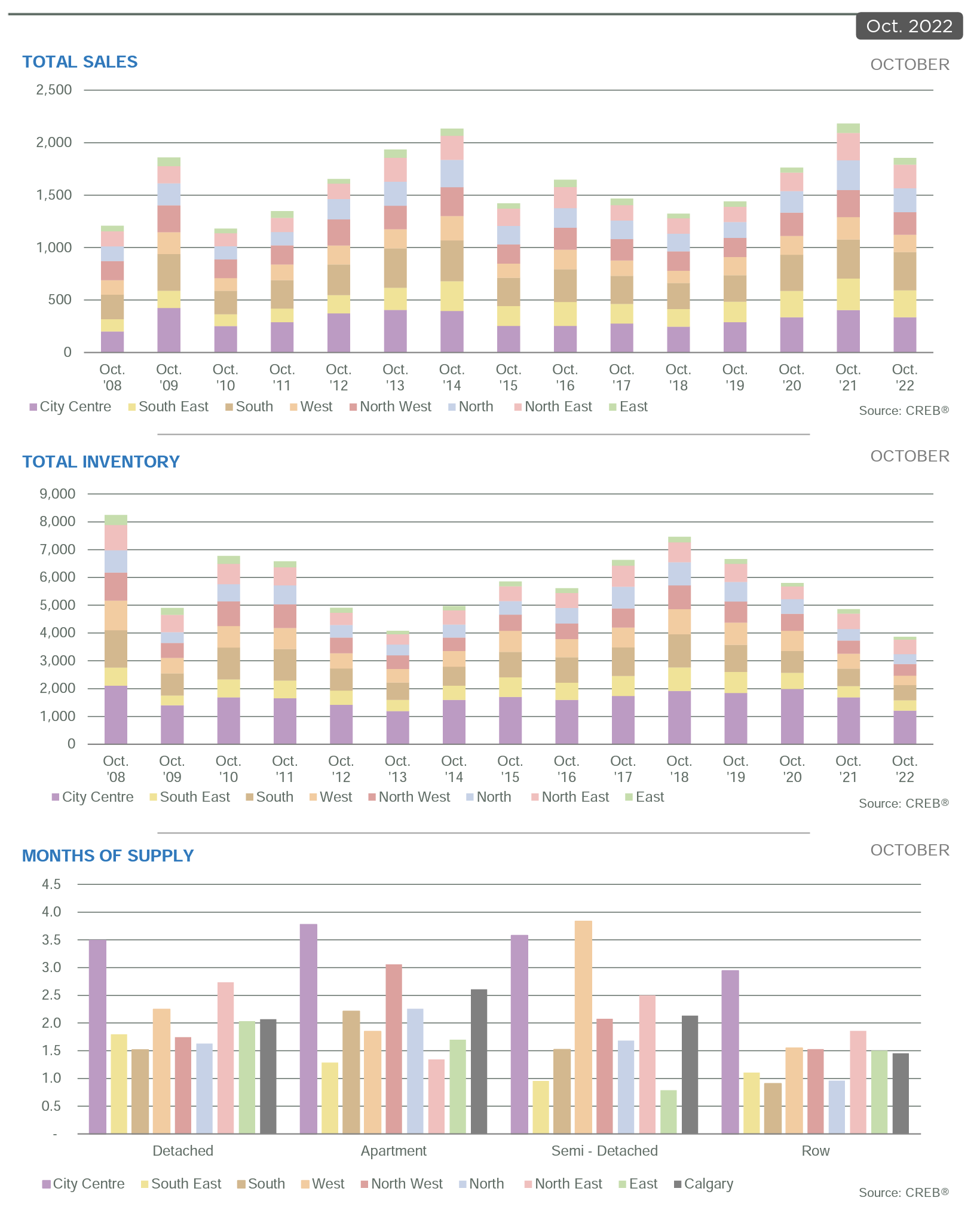

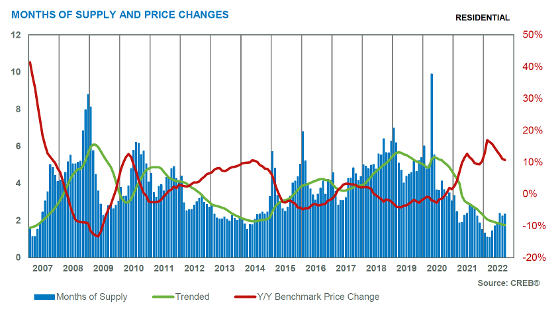

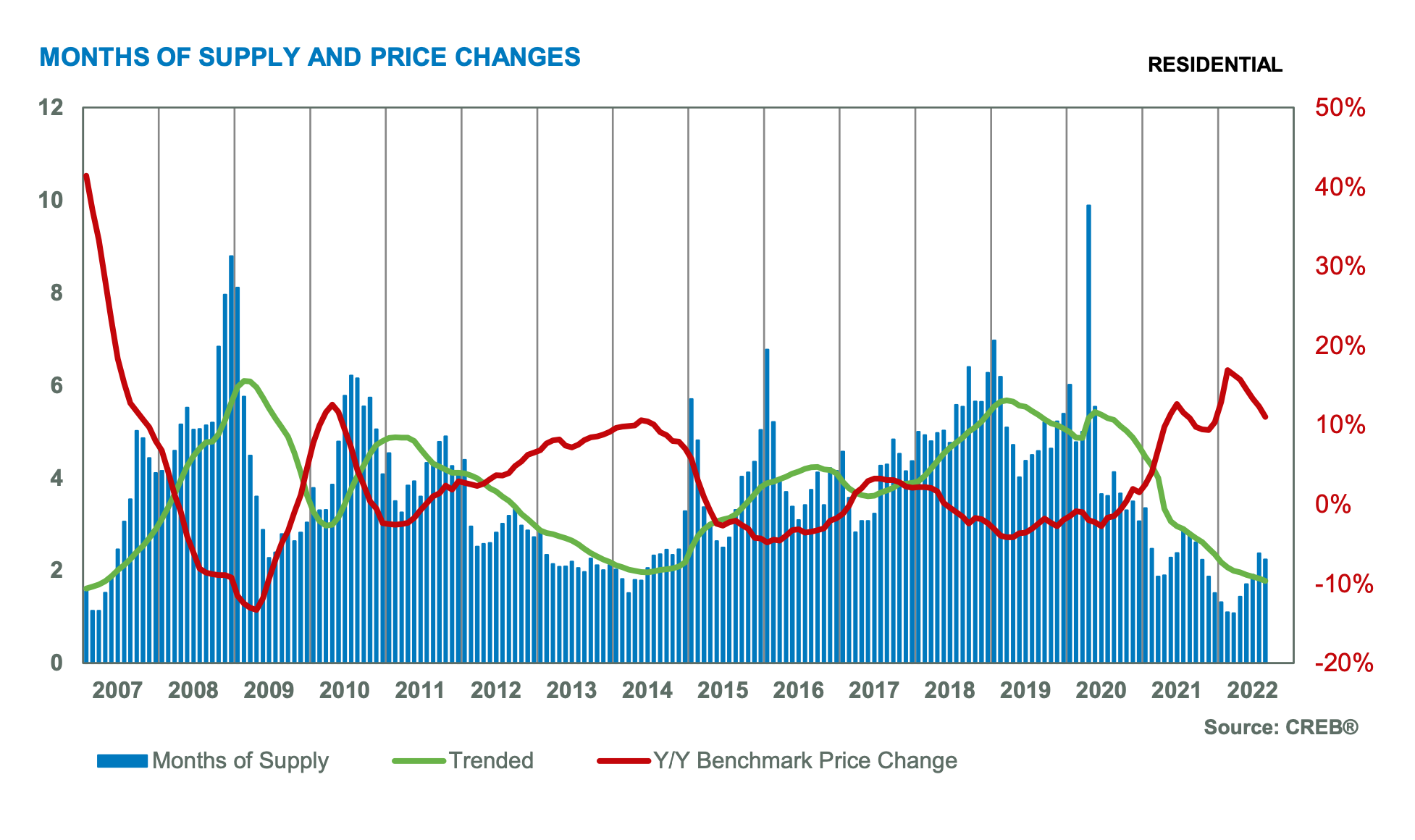

City of Calgary, October 3, 2022 –

Strong sales for condominium apartment and row properties were not enough to offset declines reported for other property types. This caused city sales to ease by nearly 12 per cent compared to last year.

However, with 1,901 sales in September, activity is still far stronger than levels achieved prior to the pandemic and is well above long-term trends for September. Despite recent pullbacks in sales, and thanks to strong levels earlier in the year, year-to-date sales remain 15 per cent higher than last year’s levels.

“While demand is easing, especially for higher priced detached and semi-detached product, purchasers are still active in the affordable segments of the market, cushioning much of the impact on sales,” said CREB® Chief Economist Ann-Marie Lurie. “At the same time, we are seeing new listings ease, preventing the market from becoming oversupplied and supporting more balanced conditions.”

In September, new listings declined by ten per cent. With a sales-to-new-listings ratio of 72 per cent, it was enough to prevent any gain in inventory levels, which declined over last month and were nearly 21 per cent lower than last year’s levels. The adjustments in both sales and supply levels have caused the months of supply to remain relatively low at less than three months.

The shift to more balanced conditions is causing some adjustments to home prices. While prices have slid from the highs seen in May, as of September, benchmark prices remain 11 per cent higher than last year and six per cent higher than levels reported at the beginning of the year.

Click here to view the full City of Calgary monthly stats package.

Click here to view the full Calgary region monthly stats package.

The interior design style known as Bauhaus is guided by the belief that materials should not be hidden behind upholstery but exposed to show the honesty of each piece.

This sparse, austere style can be recognised by its steel tubing designs of chairs, sofas and tables. It still looks incredible in modern houses and apartments, yet it rose out of a war-ravaged Germany from the 1920s.

Bauhaus elevated the skills of architecture, design and machinery and its design philosophy is around simplicity, economic logic and mass production

When you select Bauhaus as your interior design, you are embracing German history and culture that championed the beauty of industrialised, mass-produced furniture of light materials, geometric form and functionality.

Here are some tips for introducing a Bauhaus aesthetic to your home

The most fundamental of Bauhaus principles is that form follows function. Practically, this means that what looks good takes second place to practical use. For example, chairs with no discernible purpose are avoided even if one might look good in the corner of the room. This means no knick-knacks and ornaments.

Bauhaus deals faithfully with the materials of the furniture. Nothing should be hidden for the sake of aesthetics. Your home should expose the beams in the roof and make it integral to the furnishings, where the steel-tubing of chairs and tables is exposed as part of the ‘truth in materials’ philosophy.

Your entire approach must embrace the minimalist, industrial philosophy with the placement of furniture being linear. Avoid curves. Color, line and shape of furniture are the primary, almost the only, consideration in true Bauhaus design.

Bauhaus interior design inspired a new wave of German art in the early 1920s that can still be found today. The founder of the Bauhaus movement, Walter Gropius, warned against creating an empty carcass of a home and he encouraged the installation of select and powerful artwork. Everything you put in your house should embrace the overall concept of Bauhaus.

It may be the smallest room in the house, but the bathroom makes a big impact, especially with so many stunning options now available in tiling, baths and vanities.

A bathroom remodeling project can add thousands of dollars to a property and, at the same time, enhance family life. But some of the new luxury options can be a little impractical when they’re used regularly by kids.

It’s important to make great decisions that are affordable and add value to your home.

Here’s our guide to remodeling for a family-friendly bathroom that’s beautiful and practical.

A bath is essential, as every parent knows. It’s a great place to calm down the kids and get them ready for the evening and bedtime. Acrylic baths offer the best value and safer option than say, an iron bath. The new freestanding baths are the height of luxury, but with kids splashing everywhere, mess can quickly build up in hard-to-access corners. Get the best of both worlds by choosing the styles that look like they’re freestanding but actually fit flush to the wall.

Select an adjustable, detachable showerhead and hand shower to cater for every age group. It’s especially practical for washing hair and will allow you to ‘hose down’ kids on the occasions when they need it, like after a muddy sports day. Hand-helds also makes cleaning the shower easier because you can get into the corners and rinse off tiles properly.

No one enjoys scrubbing the bathroom. Reduce dust and mess build up around the S bend and awkward spots by choosing a unit that runs flush to the wall, or hangs from the wall. It will make cleaning so much easier. Also, choose a soft-closing seat to prevent it slamming down.

Make sure your vanity doesn’t have sharp edges. Avoid protruding basins as this reduces the risk of children bumping their heads. If you have space, consider installing a double vanity so there’s no fighting over the tap at teeth-brushing time. Vanity tops can be stained or scratched easily if you choose the wrong materials. Quartz and stone are high-end materials that are scratch-resistant and come in a variety of designs and colors. They’re better for high traffic and splash areas than say, timber. Glass for your shower recess and glossy porcelain tiles will maintain their original luster even with punishing usage.

Avoid the temptation to choose a white tiled floor. It will show dust, dirt and hair minutes after you’ve cleaned it. Go for a more beige or sandy color, or consider a texture that will make regular wear less noticeable. Make sure the floor tiling is non-slip. A good choice is mosaic tiling because its many grout lines offer greater grip. Tile to the ceiling if this is practical, especially behind the bath. That way the kids can splash to their hearts’ content, and you don’t have to worry about the paintwork.

Ask your bathroom designer about new devices that stop children from being scalded by hot water. A temperature-control feature in the bathroom will keep the children safe and be an asset if you wish to sell your home in the future. Easy-grip lever-handle taps can help avoid accidents, too, and they’re easier for kids to manage.

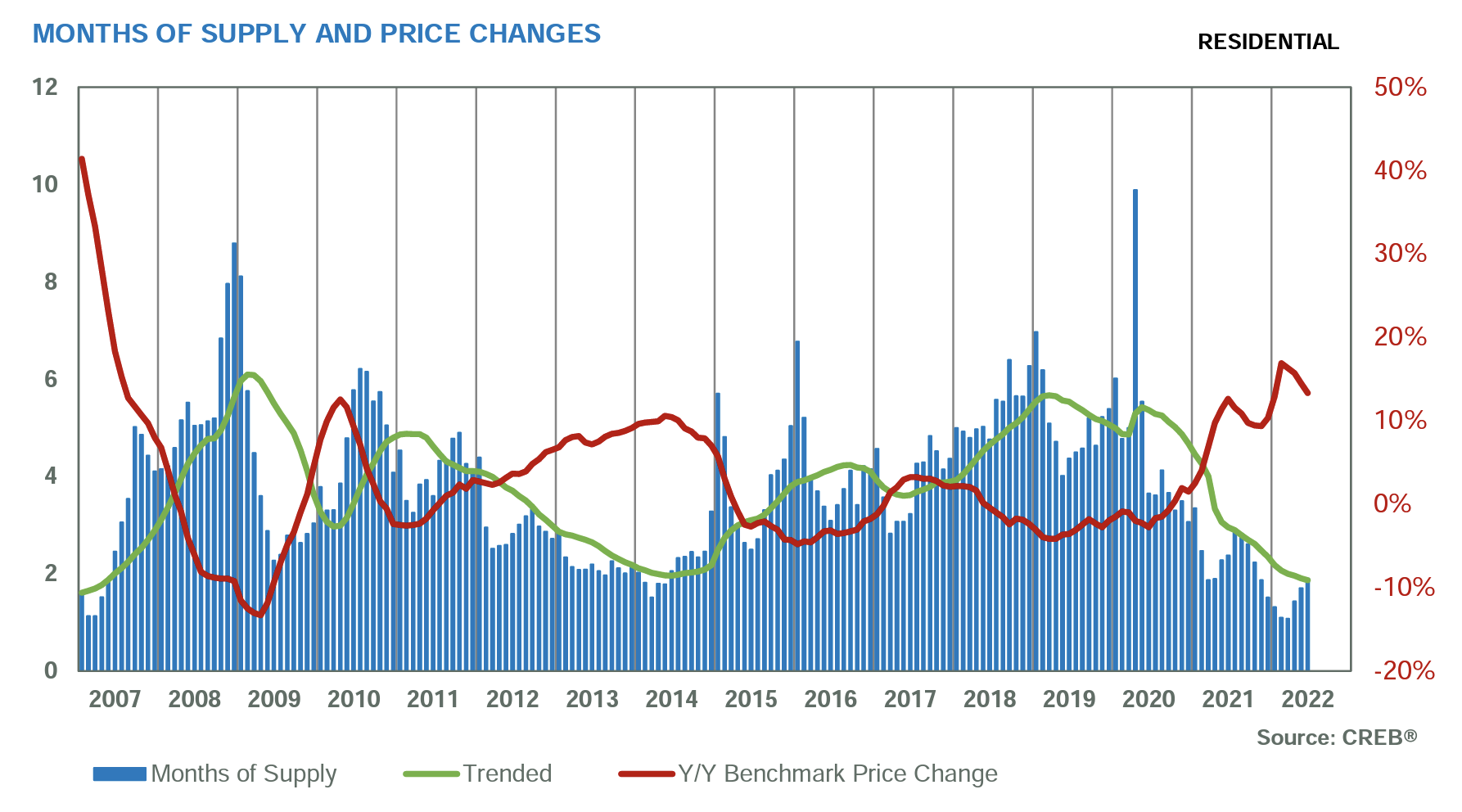

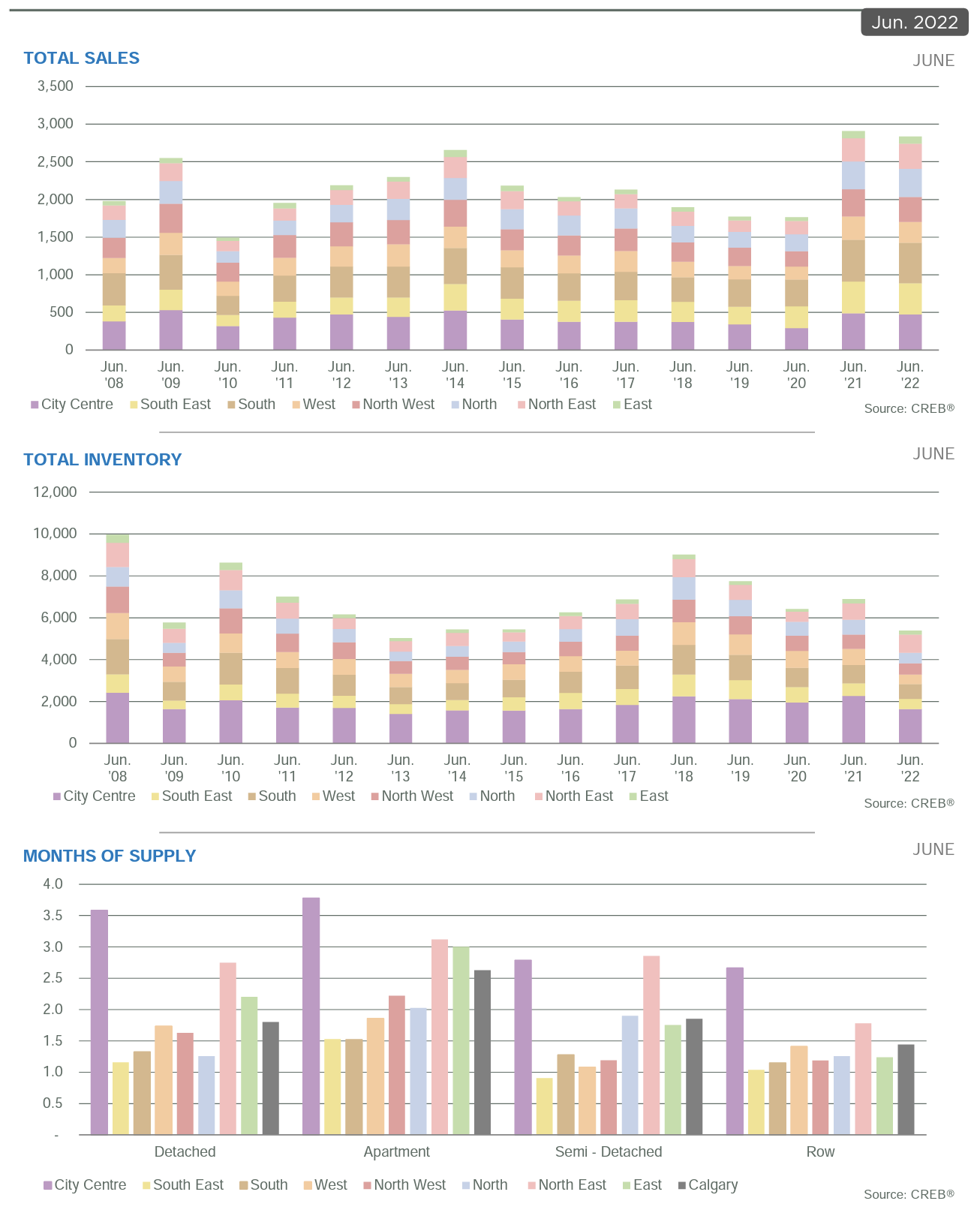

City of Calgary, July 4, 2022 – Sales activity in June eased relative to the past several months and with 2,842 sales, levels declined by two per cent over last year’s record high. While sales activity has remained relatively strong for June levels, the decline was driven by a pullback in detached and semi-detached home sales.

“As expected, higher interest rates are starting to have an impact on home sales. This is helping shift the market toward more balanced conditions and taking some of the pressure off prices,” said CREB® Chief Economist Ann-Marie Lurie.

“While we are starting to see some transition, it is important to note that in Calgary year-to-date sales are still at record levels and prices are still far above expectations for the year.”

This pullback in sales was not met with the same level of pullback in new listings. This caused inventories to trend up over previous months. These shifts are supporting some easing from the exceptionally tight conditions as the months of supply remained just shy of two months. While two months is still considered low for our market, it is a significant change over the one month of supply recorded earlier in the year.

After three months of gradual gains in the months of supply, prices eased slightly relative to last month. However, with a city-wide benchmark price of $543,900, levels are still over 13 per cent higher than last year.

With further rate gains expected, we could continue to see slower sales activity and some monthly price growth slippage in the Calgary market in the coming months. However, thanks to renewed migration and job growth in a wide range of sectors, it is unlikely that we will see a full reversal of the price gains made so far this year.

For the third month in a row, sales levels in the detached market have eased. Much of the pullback has occurred from homes priced under $600,000. While some of this is likely related to the continued lack of supply choice, the pullback in this sector is also related to the rise in lending rates that are impacting qualifications levels and creating some hesitancy among consumers.

The pullback in sales relative to new listings did cause some modest gains in inventory levels compared to earlier in the year. This helped push up the months of supply to just under two months. The shift to more balanced conditions has been limiting the upward pressure on prices. As of June, the benchmark price was $647,500. This is comparable to last month, but still 16 per cent higher than last year.

Like the detached sector, sales activity slowed in June. While the pullback in sales was not enough to offset earlier gains, it was enough to push the months of supply up to nearly two months. While this gain in months of supply is likely welcome news for some buyers, conditions still remain tight compared to what we traditionally see in this segment of the market.

Prices also saw some adjustment this month easing slightly relative to May’s levels. This was mostly due to adjustments in the North East, East, North West, North and South East districts of the city. However, with a benchmark price of $581,600, prices in Calgary remain nearly 13 per cent higher than levels reported last year.

Unlike the detached and semi-detached sector, row sales activity improved and reached a new record high for the month of June. The row market tends to offer a more affordable option for consumers compared to both semi-detached and detached homes. While new listings did improve relative to levels recorded last year, it was not enough to offset the gains in sales. As a result, inventories trended down and the months of supply remained relatively tight at one and a half months.

The benchmark price still recorded some modest gains this month, but the pace of growth slowed down significantly compared to earlier in the year. Overall, the benchmark price reached $363,700, nearly 16 per cent higher than last year.

While apartment condominium sales continued to slow from record levels reported earlier in the year, sales were still over 31 per cent higher than levels reported last year. This in part was possible due to the recent boost in new listings. At the same time, the boost in new listings did help take some of the supply pressure off this market as the sales-to-new-listings ratio eased to 62 per cent and the months of supply pushed up to nearly three months.

The shift to more balanced conditions is also helping slow the pace of price growth in this market, but not completely disrupt it. The benchmark price in June reached $277,400, nearly one per cent higher than last month and 10 per cent higher than last year’s levels. Despite these gains, prices continued to remain below 2014 highs.

Sales in June continued to ease from levels reported earlier in the year and levels achieved last year. However, the decline was not enough to offset earlier gains as year-to-date sales remain over 24 per cent above last year’s levels. While new listings did improve compared to last year, levels were not enough to significantly alter the tight market conditions in Airdrie. The sales-to-new-listings ratio remained relatively tight at 81 per cent and the months of supply, while higher than earlier in the year, pushed just slightly above one month.

Earlier in the year, Airdrie reported some of the highest monthly price gains ever seen in the market, so as interest rates rise and consumers take a step back to reevaluate conditions, it is not a surprise that we are seeing some adjustments in price. While prices have trended down for the past two months, they remain over 22 per cent higher than levels reported last year.

Easing sales this month contributed to year-to-date sales of 735 units, just slightly higher than levels reported last year. So far this year, the growth in new listings has outpaced the growth in sales and it has helped push up inventory levels relative to what was available in the market earlier in the year. This also helped push the months of supply back above one month, something that has not happened since October of last year.

While conditions remain far from balanced, the slight shift has taken some of the pressure off home prices which reported strong monthly gains earlier in the year. The benchmark price in June rose to $522,600, a slight gain over last month and nearly 18 per cent higher than prices recorded last year.

Sales activity remained relatively stable this month supporting year-to-date sales of 544 units, just slightly higher than levels reported last year. At the same time, new listings have also remained relatively consistent with last year’s levels. This is leaving the market to continue to favour the buyer with one month of supply and a sales-to-new listings ratio of 80 per cent.

Despite tight conditions, there was a modest pull back in the monthly price. However, with a benchmark price of $556,200, prices remain nearly 17 per cent higher than levels reported last year.

Click here to view the full City of Calgary monthly stats package.

Click here to view the full Calgary region monthly stats package.

City of Calgary, June 1, 2022 – For the second month in a row, sales activity trended down after all-time record high sales in March. While activity in the market slowed down in May with 3,071 sales, levels are still slightly higher than last year’s record high and are far stronger than typical levels of activity recorded in May.

“It’s not a surprise to see sales ease from the exceptionally strong levels seen earlier in the year. Many buyers were eager to get into the market ahead of the rate gains that we are now seeing,” said CREB® Chief Economist Ann-Marie Lurie.

“While higher lending rates are weighing on sales activity, the market is still struggling with supply levels and rising prices which could also be contributing to slower sales, especially in the detached market. Nonetheless, if this shift continues, we could begin to see more balanced conditions in the market over the next several months, slowing the pace of price growth in the market.”

Slower sales were met with a decline in new listings, but a strong pullback in sales was enough to cause inventories to trend up relative to levels seen over the past few months. While inventory remains well below historical norms, the monthly gains did take off some of the pressure in the market. However, with just under two months of supply, the market continues to favour the seller.

Tight market conditions continue to contribute to further price gains in the market, but the pace of growth has eased relative to what occurred over the previous four months. Overall, the benchmark price reached $546,000 in May, over 14 per cent higher than last year’s levels.

Benchmark home prices reflect a typical home to ensure price movements better reflect market activity. Over time, the typical home evolves and the MLS® Home Price Index also evolves to ensure the data remains in line with modern housing trends. As of today, the benchmark price was recalculated based on a modern typical home. Details on the model adjustments can be found on the Canadian Real Estate Association’s website.

Higher lending rates, steep price gains and exceptionally tight conditions in the market are starting to weigh on consumers and contributing to the pullback in detached sales this month. Sales trended down in all locations except the most affordable North East and East markets in the city, which continue to record sales growth. Slower sales were met with a pullback in new listings which prevented any steep gains in inventory levels. With 2,552 units in inventory and 1,620 sales, the months of supply edged up over last month but continues to favour the seller.

Persistently tight conditions did contribute to further price gains this month, but the pace of growth has eased compared to earlier in the year. Detached benchmark prices reached $648,500 in May, nearly 17 per cent higher than last year. Year-over-year gains have occurred across all districts with the gains ranging from a low of 10 per cent in the City Centre to over 22 per cent in the South East and North East.

Like the detached sector, sales slowed this month for semi-detached properties. However, sales still remain relatively strong and on a year-to-date basis are still higher than levels recorded last year. New listings also slowed, but at a slower pace than sales causing some modest monthly gains in inventory levels and some monthly gains in the months of supply. However, with less than two months of supply, this segment continues to favour the seller.

While prices continued to rise for semi-detached properties, the pace of growth has eased from earlier in the year. In May, the semi-detached benchmark price reached $584,700, nearly 15 per cent higher than the same time last year. Price gains have occurred across all districts with the strongest year-over-year gain occurring in the North district of the city.

Like other property types, sales activity trended down from the March high. However, sales in May were still higher than last year’s levels and reflect a new record high for May. Row properties in the city are generally more affordable than both detached and semi-detached properties. Higher prices in other sectors and rate gains are likely driving more consumers toward row style properties.

While some monthly gains in inventories did help push up the months of supply, with 1.5 months of supply conditions continue to favour the seller. The persistently tight conditions placed further upward pressure on prices, however, the pace of growth is easing. As of May, the benchmark price reached $363,300, nearly 17 per cent higher than last year’s levels.

Recent gains in sales and prices likely encouraged the boost in new listings this month for apartment condominiums. While sales did improve significantly compared to last year, the sales-to-new-listings ratio eased to 67 per cent and inventories edged up over relative to levels seen over the past five months. This rise was enough to push up the months of supply to over two months. While this segment of the market has been more sensitive to supply shifts, conditions still remain relatively tight supporting further price gains.

The benchmark price in May reached $275,300, over one per cent higher than last month and nearly nine per cent higher than last year. Prices trended up in every district helping support price recovery. Despite the growth, prices are still over 10 per cent below the highs set back in 2014.

For the first time in nearly two years, sales in Airdrie eased over last year’s levels. Meanwhile, the new listings in the market remained comparable to last month but were slightly better than last year’s levels. This helped push inventories and the months of supply up compared to last month. However, with the months of supply remaining at one month, the market remains exceptionally tight.

Despite tight market conditions, we did see prices take a pause this month, easing slightly over last month but remaining nearly 25 per cent higher than levels recorded last year. Prices have been trending up monthly for the better part of two years and the growth at the start of this year has far exceeded expectations. As rates continue to rise and the market shifts to more balanced conditions, we expect the pace of the price growth to start to slow.

Sales in Cochrane continued to remain strong in May, supporting a year-to-date annual gain of nearly seven per cent. While we have seen some signs of improvement in new listings, that was not the case this month. The sales-to-new-listings ratio rose to 98 per cent, higher than levels seen over the past four months. With no additions to the inventory in the market, the months of supply remained below one month. This supported persistent sellers’ market conditions.

The tight conditions continue to place upward pressure on prices. However, the pace of growth is starting to slow as May prices were 18 per cent higher than last year’s levels. Price growth remains the strongest for detached and semi-detached properties with year-over-year gains pushing 21 per cent.

Sales remained relatively strong this month, contributing to a year-to-date gain of nearly 17 per cent. This growth was possible as new listings did improve this month. However, with an 87 per cent sales to new listings ratio and a months of supply remaining below one month, conditions continue to remain relatively tight in this market.

The benchmark price reached $560,700 in May. This is a significant jump over last month and 19 per cent higher than last year’s levels. Like most locations, much of the gain is being driven by the detached sector of the market, which saw prices push up to $625,200 this month.

Click here to view the full City of Calgary monthly stats package.

Click here to view the full Calgary region monthly stats package.

Sellers' market conditions continue in April

City of Calgary, May 2, 2022 – Following an all-time record high month of sales in March, activity slowed down in April. However, with 3,401 sales, it was still a gain of six per cent over last year and a record high for the month of April.

“Despite some of the monthly pullback, it is important to note that sales remain exceptionally strong and are likely being limited due to supply choice in the market,” said CREB® Chief Economist Ann-Marie Lurie. “While further rate increases will likely start to dampen demand later this year, more pullbacks in new listings this month are ensuring the market continues to favour the seller, resulting in further price gains."

New listings trended down relative to last month and levels recorded last year. With the sales-to-new listings ratio remaining above 74 per cent, there was not much of a shift in overall inventory levels.

With 4,850 units in inventory, we are nowhere near record low inventory levels, however, levels are far lower than what was recorded in April since 2014. What has changed in the market is the composition of the inventory levels. When comparing inventories today to what was available in 2014, we can see that detached homes comprise of a smaller share of the inventory levels especially for properties priced below $500,000.

Overall, the Calgary market has seen the months of supply remain below two months since November of last year, placing significant upward pressure on prices. The benchmark price in April reached $526,700, which is nearly two per cent higher than last month and 17 per cent higher than last year.

Detached

For the first time since spring of 2020, year-over-year sales slowed down. While sales have dropped, it is important to note that with 1,815 sales, this is still far stronger than long term trends. A decline in sales occurred for homes priced under $600,000. This pullback in sales for lower priced homes was likely related to further supply declines driven from reductions in new listings in those price ranges. Inventories in the detached sector have not been this low for the month of April in nearly 15 years.

While the slightly slower sales compared to inventory levels did help push the months of supply back above one month, conditions continue to remain exceptionally tight with 1.3 months of supply. This continues to place upward pressure on prices, but at a slower pace than the last three months. The detached benchmark price rose to $628,900 in April, which is 19 per cent higher than last year.

Semi-Detached

A decline in new listings in April likely contributed to slower sales compared to last month. However, sales are still relatively strong and on a year-to-date basis and remain nearly 30 per cent higher than last year and nearly double the long-term average. As the slower pace of sales was met with a decline in new listings, there was little change in the inventory situation and this segment continues to favour the seller.

Tight market conditions caused further price gains in the semi-detached sector. In April, the benchmark price reached $487,900, nearly two per cent higher than last month and over 16 per cent higher than last April.

Row

While levels trended down from the previous month, new listings reached 781 units this month. This is a year-over-year gain of 24 per cent and the highest level ever seen in April. The improvements in new listings helped support stronger sales activity which rose over last year’s levels and set a new April high. This boost in new listings did cause inventories to trend up compared to earlier in the year, but it was not enough to pull the market out of the sellers’ market conditions.

With just over one months of supply, persistently tight market conditions continue to place upward pressure on prices. Thanks to gains across every district, row prices rose by over two per cent compared to last month and are nearly 17 per cent higher than last year.

Apartment Condominium

Like other property types, apartment condominium sales did ease relative to last month’s record highs. But with 642 sales this month, activity still improved by over 46 per cent compared to last year reaching a record high for April. This in part was possible thanks to the 893 new listings that came onto the market. While it was not enough to dramatically change the supply levels in the market, the months of supply did edge up to nearly two months.

Tighter market conditions continued to cause prices to trend up in April. The apartment benchmark price rose across all districts and currently sits eight per cent higher than levels recorded at this time last year. The strong price gains over the past three months have helped narrow the spread from the 2014 record high price.

REGIONAL MARKET FACTS

Airdrie

Once again, sales nearly surpassed the level of new listings coming onto the market in April, causing further declines in inventory levels and ensuring the market continues to favour the seller with less than one month of supply. This is the sixth consecutive month where the months of supply has remained below one month.

The benchmark price reached $480,600 in April, reflecting a year-over-year gain of 29 per cent. Prices have improved across all property types, but the largest gains are in the detached sector with an April price pushing just above $550,000. This is nearly 33 per cent higher than levels recorded last April.

Cochrane

A slight pullback in sales relative to the new listings helped push the sales-to-new listings ratio below 80 per cent. This is the first time that has happened since March of last year. While this did support inventory levels that were better than anything seen since November of last year, conditions still remain exceptionally tight and favour the seller.

While the pace of growth has slowed slightly compared to the last few months, the April benchmark price in Cochrane reached $530,900, over two per cent higher than last month and 21 per cent higher than last year’s levels. Price gains in Cochrane have been driven mostly by the detached and semi-detached sector.

Okotoks

The boost in new listings last month did not continue this month, as April sales exceeded the number of new listings coming onto the market. This caused further declines in inventory levels and the months of supply. This is the fifth consecutive month where the months of supply was below one month, which is continuing to weigh on prices.

The benchmark price in April rose to $538,300, reflecting a year-over-year gain of 13 per cent. Like many other areas, the strongest price growth has occurred for both detached and semi-detached homes.

Click here to view the full City of Calgary monthly stats package.

Click here to view the full Calgary region monthly stats package.

City of Calgary, April 22, 2022 –

For the full report, please download CREB®’s Q1 2022 Calgary & Region Quarterly Update Report here.

The first quarter of 2022 saw record high sales activity, thanks to an increase in new listings. This provided some choice for buyers in comparison to the previous quarter, where sales exceeded the number of new listings.

Although there was an improvement in new listings, it was not enough to add significant supply to the market. Inventory levels declined over the last quarter of 2021 and were 30 per cent lower than long-term trends, reflecting the lowest quarterly inventory level seen since 2014.

“Record sales combined with low inventory levels caused the months of supply to average just over one month in the first quarter,” said CREB® Chief Economist Ann-Marie Lurie.

“Conditions have not been this tight since 2006, which was also the last time that we saw price gains push above 15 per cent.”

The persistent sellers’ market conditions weighed on prices in the first quarter of 2022. Driven by strong gains in the detached sector of the market, the total residential benchmark price averaged $496,767. This is a quarterly gain of nearly eight per cent and a year-over-year gain of over 15 per cent.

While sales were expected to be strong in the first quarter, demand continued to exceed expectations.

“Expectations on rising rates and further price gains is likely pushing consumers to enter the market as soon as possible,” said Lurie.

“However, lack of choice over the past several quarters has created a build up of demand that can only be filled as supply levels improve.”

While economic improvements will continue to support housing demand, this pace of sales is still expected to cool later this year. This will eventually help the market shift to more balanced conditions and slow the upward pressure on prices.

March 3, 2025 Sales remain above long-term trends despite declines Inventory levels saw substantial year-over-year ...

Supply levels improve in January Calgary, Alberta, February 3, 2025 – Following three consecutive years ...